Home loan as leverage

Let's say someone has the cash to pay fully for a house. Assuming that he's not risk averse and just interested in generating good investment rate of return, should he pay fully or get a home loan and invest the rest of cash in, say, shares? If further assuming that there's little fluctuation in interest rate and investment rate of return on share price, then the answer is pretty obvious.

However, from my experience, not many people realise this. Hence, I set out the example below to show the answer.

Setting

Cash = $400,000

House price = $400,000

House price appreciation = 10% p.a.

Rental yield = 4% p.a.

Share price appreciation = 7% p.a.

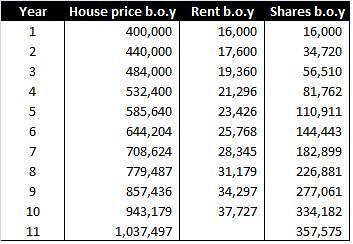

Option 1

Use cash to buy house. Rent received is invested in shares.

b.o.y = beginning of year

Investment value at the end of 10 years = $1,395,072

Investment rate of return = 13.3% p.a.

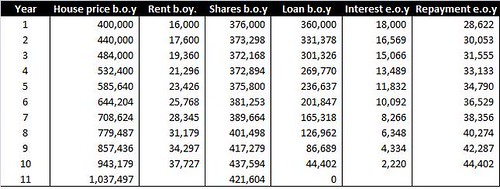

Option 2

Use 10% cash and 90% home loan (over 10 years) to buy house. Rent received is invested in shares. Shares are liquidated if needed to pay the loan instalment.

Home loan interest rate = 5% p.a.

Yearly instalment = $46,622

e.o.y = end of year

Investment value at the end of 10 years = $1,459,101

Investment rate of return = 13.8% p.a.

Conclusion

Hence, the answer is to take the home loan. In fact, there is no need to consider rent because it is applicable to both options. For the same reason, there is no need to consider expenses relating to the house e.g. maintenance and taxes.

The key factor is whether home loan is borrowed or not. The difference in the investment rate of return between the 2 options in the example above is 0.5% p.a. This difference will be larger the greater the gap between the investment rate of return on the share price and the home loan interest rate.

Summary

In deciding whether you should use cash or take a home loan, you may want to consider taking the home loan if you are able to generate a return on your cash that is at a higher rate than the home loan interest rate.

Update: the above points are also applicable when deciding how much loan to take e.g. 90% or 80% and also when deciding whether to make partial prepayment in the future.

However, from my experience, not many people realise this. Hence, I set out the example below to show the answer.

Setting

Cash = $400,000

House price = $400,000

House price appreciation = 10% p.a.

Rental yield = 4% p.a.

Share price appreciation = 7% p.a.

Option 1

Use cash to buy house. Rent received is invested in shares.

b.o.y = beginning of year

Investment value at the end of 10 years = $1,395,072

Investment rate of return = 13.3% p.a.

Option 2

Use 10% cash and 90% home loan (over 10 years) to buy house. Rent received is invested in shares. Shares are liquidated if needed to pay the loan instalment.

Home loan interest rate = 5% p.a.

Yearly instalment = $46,622

e.o.y = end of year

Investment value at the end of 10 years = $1,459,101

Investment rate of return = 13.8% p.a.

Conclusion

Hence, the answer is to take the home loan. In fact, there is no need to consider rent because it is applicable to both options. For the same reason, there is no need to consider expenses relating to the house e.g. maintenance and taxes.

The key factor is whether home loan is borrowed or not. The difference in the investment rate of return between the 2 options in the example above is 0.5% p.a. This difference will be larger the greater the gap between the investment rate of return on the share price and the home loan interest rate.

Summary

In deciding whether you should use cash or take a home loan, you may want to consider taking the home loan if you are able to generate a return on your cash that is at a higher rate than the home loan interest rate.

Update: the above points are also applicable when deciding how much loan to take e.g. 90% or 80% and also when deciding whether to make partial prepayment in the future.

Comments

Some average joes may be considering whether they want to make partial prepayment when they receive a lump sum e.g. bonus, as some home loan allows such prepayment without penalty. So the points presented in this post are also applicable in such cases. Also applies to cases where someone is deciding, say, whether to take 90% or 85% home loan.

Hmmm ok, I've amended the post to indicate that the points also applicable to other scenarios. I believed it's quite important to know this because home loan is the cheapest loan one will ever get from banks.

"Money can't buy happiness, but it sure makes misery easier to live with." sr

Actually, it doesn't matter whether interest rate stays low or not. What matters is the gap between the investment rate of return and the interest rate. The higher the rate of return over the interest rate, the safer it is.

sr,

Yes, there are a host of factors to consider too e.g. fluctuation of the difference between the invest rate of return and interest rate, the possibility of market value of the house plunging below the value of the outstanding loan, possibility of being unemployed. This is why I'm a little cautious in my conclusion ("...may want to consider...") However, this post would need to be much longer to address these. Also, I believed most people are aware of these factors but not the points I'm raising in this post.

The purpose of this post is to discuss the choice between forking out cash to buy property or getting or a home loan for the same purpose. Since the your scenario has no cash component, it's a different case. I'm not sure what you're asking.